Understanding Section 44AD of Income Tax Act

Understanding Section 44AD of Income Tax India 1961

Section 44AD of the Income Tax Act is a presumptive taxation scheme designed for eligible small businesses, professionals, and freelancers. It allows taxpayers to declare their income at a prescribed rate without maintaining detailed accounting records or undergoing complex tax assessments. This simplified approach aims to reduce compliance burdens and promote ease of doing business for small enterprises.

Eligibility for Section 44AD

Section 44AD is applicable to certain resident individuals, Hindu Undivided Families (HUFs), and partnerships (excluding LLPs) that meet the following criteria:

The total turnover or gross receipts of the business should not exceed Rs. 3 crores in a financial year.

The taxpayer should be engaged in a specified business, such as civil construction, brokerage, commission agency, or any other notified business.

The taxpayer should not have claimed deductions under sections 10A, 10AA, 10B, 10BA, or 80HH to 80RRB.

Certain specified professions such as doctors, lawyers, engineers, architects, and consultants are also eligible under Section 44AD.

Calculation Method - Tax Deductions and Income Declarations

Under Section 44AD, the presumptive income is computed as follows:

For businesses providing professional or non-professional services: 50% of gross receipts or turnover

For businesses involving the sale, manufacturing, or trading of goods:

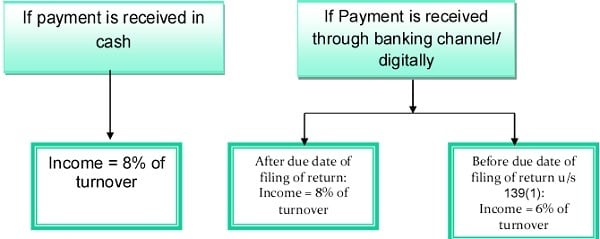

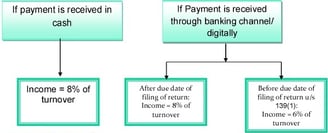

8% of gross receipts or turnover if payment is received in cash.

6% of gross receipts or turnover if payment is received digitally.

Taxpayers opting for Section 44AD simply declare their income at these prescribed rates, irrespective of their actual expenses or profits.

It is important to note that eligible taxpayers declaring income under Section 44AD are not required to maintain regular books of accounts or get them audited. This provision simplifies the tax compliance process for small businesses and reduces the burden of maintaining extensive financial records.

Benefits of Section 44AD

Simplified Tax Calculation: Under Section 44AD, eligible taxpayers can declare their income at a presumptive rate, which is a percentage of their gross receipts or turnover. This eliminates the need for maintaining detailed books of accounts and calculating business profits based on actual expenses.

Reduced Compliance Burden: The provision eliminates the need for maintaining detailed books of accounts and getting them audited, which saves time and resources. This reduces compliance costs and administrative burdens for small businesses and professionals.

Presumptive Taxation: By opting for Section 44AD, taxpayers enjoy the benefit of presumptive taxation, which simplifies the tax filing process.

Higher Profit Margin: The prescribed rate under Section 44AD is generally lower than the actual profit margin, allowing taxpayers to retain a higher portion of their income.

Lower Tax Liability: The presumptive rates under Section 44AD are generally lower than the actual tax rates applicable to business profits. This results in a lower tax liability for eligible taxpayers, enhancing their cash flow and financial viability.

Other Key Considerations:

While Section 44AD offers significant benefits, taxpayers should consider the following factors:

Optimal Tax Planning: Evaluate whether declaring income under Section 44AD is more beneficial than actual profit computation, especially if actual expenses are lower than the presumptive rates.

Compliance Requirements: Ensure compliance with other provisions of the Income Tax Act, such as maintaining basic financial records, filing tax returns, and fulfilling other statutory requirements.

It is important to consult a tax professional or chartered accountant to understand the applicability and implications of Section 44AD based on your specific business circumstances.

In conclusion, Section 44AD of the Income Tax Act provides a simplified scheme for calculating taxable income for eligible taxpayers. By understanding the eligibility criteria, tax deductions, income declarations, and benefits associated with this provision, taxpayers can streamline their tax filing process, reduce tax liabilities, and ensure compliance with the law.