Factors That Impact CIBIL Scores and How to Avoid a Poor Score

In the realm of personal finance, few things hold as much sway over one's financial health as the elusive CIBIL score. This three-digit number, ranging from 300 to 900, serves as a barometer of an individual's creditworthiness, influencing their ability to secure loans, credit cards, and other financial products. But what factors contribute to this all-important score, and how can individuals ensure their score remains favorable? In this article, we'll explore the key factors that impact the CIBIL score and provide insights into maintaining a healthy credit profile.

1. Payment History: The most significant factor influencing your CIBIL score is your payment history, accounting for approximately 35% of the score. Timely repayment of credit card bills, loan EMIs, and other debts demonstrates financial responsibility and reliability to lenders, positively impacting your score.

2. Credit Utilization Ratio: Your credit utilization ratio, or the amount of credit you use compared to your total available credit, plays a crucial role in determining your CIBIL score. Ideally, you should keep this ratio below 30% to avoid being perceived as overly reliant on credit and to maintain a favorable score.

3. Length of Credit History: The length of your credit history accounts for about 15% of your CIBIL score. Lenders prefer borrowers with a long and established credit history, as it provides insights into their credit behavior over time. Therefore, maintaining older credit accounts and avoiding frequent closures can positively impact your score.

4. Credit Mix: Having a diverse mix of credit accounts, such as credit cards, loans, and retail accounts, can positively influence your CIBIL score. This demonstrates your ability to manage different types of credit responsibly and adds depth to your credit profile.

5. New Credit Inquiries: Each time you apply for new credit, lenders conduct a hard inquiry on your credit report, which can temporarily lower your CIBIL score. Therefore, it's essential to limit the number of credit inquiries and avoid applying for multiple credit accounts within a short period.

6. Credit Account Age: The age of your credit accounts also factors into your CIBIL score. Older accounts with a history of timely payments contribute positively to your score, while newly opened accounts may initially have a minimal impact.

7. Negative Items: Negative items such as late payments, defaults, foreclosures, and bankruptcies can significantly damage your CIBIL score and remain on your credit report for several years. It's crucial to address and resolve these issues promptly to minimize their impact on your creditworthiness.

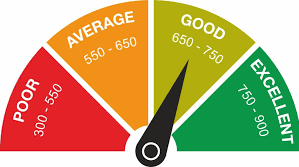

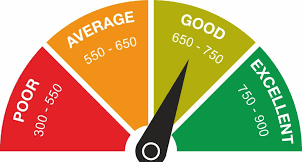

What is a good cibil score?

Any score above 750 is considered as an excellent score, which would mean lower interest rates and high profile, whereas any score below 550 is considered as poor score. The above charts explains these ranges in detail.

Maintaining a healthy CIBIL score is essential for accessing credit on favorable terms and achieving financial goals. By understanding the factors that impact your score and adopting responsible credit management practices, you can enhance your creditworthiness and secure a brighter financial future. Regularly monitoring your credit report and taking proactive steps to address any discrepancies or negative items can help you maintain a favorable CIBIL score over time.