Comparing the Old and New Tax Regimes in India

The tax regime in India has recently undergone a significant change with the introduction of the new tax regime. This has sparked a debate among taxpayers about which regime is more beneficial for them. In this article, we will compare the old tax regime with the new tax regime and analyze the advantages and disadvantages of each.

Old Tax Regime

The old tax regime in India follows a progressive tax structure, where individuals are taxed at different rates based on their income slabs. It allows taxpayers to claim various deductions and exemptions under Section 80C, 80D, 80G etc. of the Income Tax Act. These deductions include deductions for investments in instruments such as Provident Fund (PF), Public Provident Fund (PPF), Equity Linked Savings Scheme (ELSS), life insurance premiums, medical insurance premiums, etc.

Under the old regime, taxpayers can avail of deductions for allowances for house rent, medical expenses, education loans, and more.

One of the key advantages of the old tax regime is the ability to claim these deductions, which can significantly reduce the taxable income. This can result in lower tax liability for individuals who have substantial deductions.

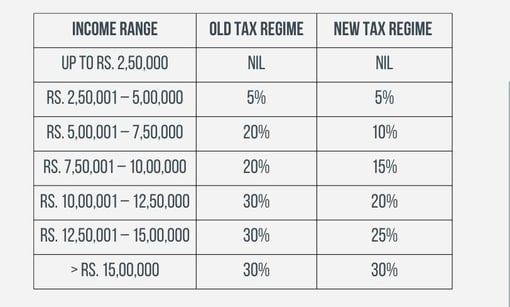

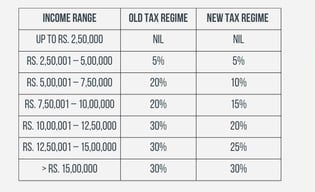

The tax rates under the old regime range from 5% to 30% depending on the income slab, with additional cess and surcharge applicable for higher income brackets.

However, the old tax regime can be complex and time-consuming to navigate. Taxpayers need to keep track of various deductions and exemptions and maintain supporting documents for the same. This can be a hassle, especially for individuals with multiple sources of income or those who frequently change jobs.

The choice between the old tax regime and the new tax regime in India depends on individual circumstances, financial preferences and goals. While the old regime allows for more deductions and exemptions, the new regime offers a simplified tax filing process and lower tax rates. It is important for taxpayers to carefully evaluate their financial situation and consider factors such as income, deductions, and personal preferences before deciding which tax regime to opt for.

New Tax Regime

The new tax regime, introduced in 2020, offers a simplified tax structure with lower tax rates. Under this regime, taxpayers are not allowed to claim most deductions and exemptions available in the old tax regime. Instead, they are subjected to a flat tax rate based on their income slabs and the tax rates range from 5% to 30% without any deductions.

The new tax regime aims to simplify the tax filing process and reduce the compliance burden on taxpayers. It eliminates the need to keep track of various deductions and exemptions, making tax filing less complicated and time-consuming.

However, the trade-off for the simplicity of the new tax regime is the inability to claim deductions and exemptions. This means that individuals who have significant deductions under the old regime may end up paying more taxes under the new regime.

Which is More Beneficial?

The answer to whether the old tax regime or the new tax regime is more beneficial depends on individual circumstances. For individuals with substantial deductions and exemptions, the old tax regime may result in lower tax liability.

On the other hand, individuals with minimal deductions or those who prefer a simplified tax filing process may find the new tax regime more beneficial. The lower tax rates in the new regime can result in overall tax savings for such individuals.